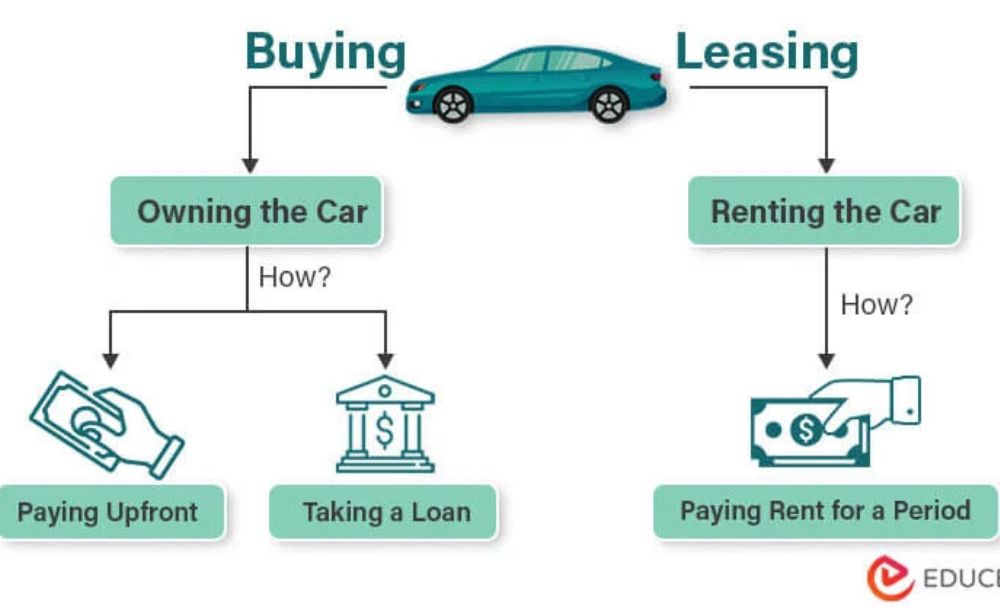

Car finance agreements have become an essential part of the vehicle market in the UK. For many drivers, they offer a convenient way to spread the cost of a car without having to pay a large sum upfront. One of the most popular forms of finance is personal contract purchase, commonly known as PCP.

At first glance, PCP deals seem like an ideal solution for those seeking flexibility and affordability. However, beneath the surface, some agreements include hidden costs that many drivers only discover after it’s too late. These hidden charges, unclear terms, and undisclosed commissions are now leading more drivers to take action through car finance claims.

If you’re considering a car finance agreement — or already have one — understanding these claims from a smart money perspective can help you protect yourself and avoid costly mistakes. Here’s everything you need to know.

Why Car Finance Claims Are Making Headlines

Personal contract purchase agreements were designed to make car finance more accessible. With lower monthly payments and options to buy, return, or trade in the car at the end of the contract, PCP deals have long been a popular choice.

However, recent investigations have revealed that not all agreements have been as fair as they should be. Many drivers have been caught out by hidden costs, commissions that were never disclosed, and complex terms that were difficult to understand.

These issues have led to a significant rise in PCP claims. Drivers are now questioning whether they were misled or overcharged — and many are discovering they have grounds to seek compensation.

What Hidden Costs Might Be Lurking in Your Agreement?

Spotting hidden costs can be tricky, especially when finance agreements are often packed with technical language. However, there are several common areas where drivers may face unexpected charges or unfair terms.

Here are some of the most frequent hidden costs linked to PCP agreements:

1. Undisclosed Commission Payments

Some brokers or dealerships may have received commissions from finance providers without informing customers. These payments can sometimes lead to higher interest rates, increasing the overall cost of the agreement.

2. Balloon Payments

At the end of a PCP agreement, drivers must pay a final lump sum to own the car. This balloon payment can be far higher than expected, leaving drivers unable to afford it.

3. Mileage Limits and Penalties

Most PCP deals come with strict mileage limits. Exceeding these limits can result in significant penalties, which are not always clearly explained upfront.

4. Wear and Tear Charges

Returning the vehicle may lead to extra charges for any damage deemed beyond “fair wear and tear”. This can include minor scuffs or dents that seem unavoidable during everyday use.

How to Spot If You’ve Been Affected

Identifying whether your car finance agreement may have been unfair isn’t always straightforward, but there are some clear warning signs to watch out for.

Consider reviewing your agreement if:

- You were not informed about any commissions or fees linked to your finance deal.

- Your interest rate seems higher than expected, without a clear explanation.

- You faced pressure to sign the agreement without enough time to review the terms thoroughly.

- You’re struggling with unexpected costs, such as balloon payments or penalties, that were not fully explained at the start.

If any of these points apply to you, it may be worth seeking professional advice to review your agreement in detail.

Why PCP Refunds Are Becoming More Common

The growing awareness of hidden costs in car finance deals has led to a notable rise in drivers seeking refunds. A PCP refund claim allows drivers to recover some of the money they paid as a result of unfair or mis-sold agreements.

Drivers who signed PCP agreements between 2007 and 2021 are now eligible to explore the possibility of a refund if they were not clearly informed about key aspects of their deal, such as undisclosed commissions or inflated interest rates.

Making a claim typically involves reviewing your agreement, gathering supporting documents, and submitting the necessary paperwork to the relevant claims service or legal professional.

Many drivers are now pursuing compensation not only to recover lost money but also to hold finance providers accountable for unfair practices.

Why Car Finance Claims Are Here to Stay

There are several reasons why car finance claims are likely to remain a key issue in the UK’s consumer finance market:

- Widespread Use of PCP Deals: With PCP being one of the most popular car finance options, many drivers could potentially be affected.

- Increased Public Awareness: Media coverage and online discussions have brought the issue to light, encouraging more people to review their agreements.

- Easy Access to Claims Tools: Digital claims platforms make it easier for drivers to check eligibility and start a claim without complicated paperwork.

- Consumer Protection Focus: Growing emphasis on fair treatment and transparency in financial services is driving further scrutiny of car finance agreements.

How to Protect Yourself Before Signing Any Car Finance Deal

If you’re thinking about taking out a car finance agreement, it’s important to approach the process with caution and confidence. Here are some smart money tips to help you protect yourself:

- Ask Direct Questions: Make sure to ask about commissions, fees, and the total cost of borrowing before signing.

- Review the Terms Thoroughly: Read every part of the agreement and look out for terms related to balloon payments, mileage limits, and early exit penalties.

- Compare Options: Don’t rely solely on the dealer’s offer — shop around and compare finance deals from different providers.

- Take Your Time: Never feel rushed into signing. If necessary, take the agreement home to review it properly.

- Seek Independent Advice: If you’re unsure about the terms, consult an independent financial adviser before committing.

Final Thoughts

Car finance agreements can provide flexibility and affordability, but they also come with risks that every driver should understand. Hidden costs, undisclosed commissions, and complicated terms can quickly turn a seemingly good deal into a financial burden.

By learning how to identify these pitfalls and seeking professional advice when needed, drivers can take control of their finances and avoid unpleasant surprises.

If you signed a PCP agreement between 2007 and 2021 and suspect that you were not given full information, you may be eligible to make a PCP claim. Many drivers are already reviewing their agreements and filing claims to recover money through refunds or compensation.

As awareness continues to grow, more people are discovering that being informed is the first step toward protecting their financial wellbeing — and ensuring fair treatment in the car finance market.